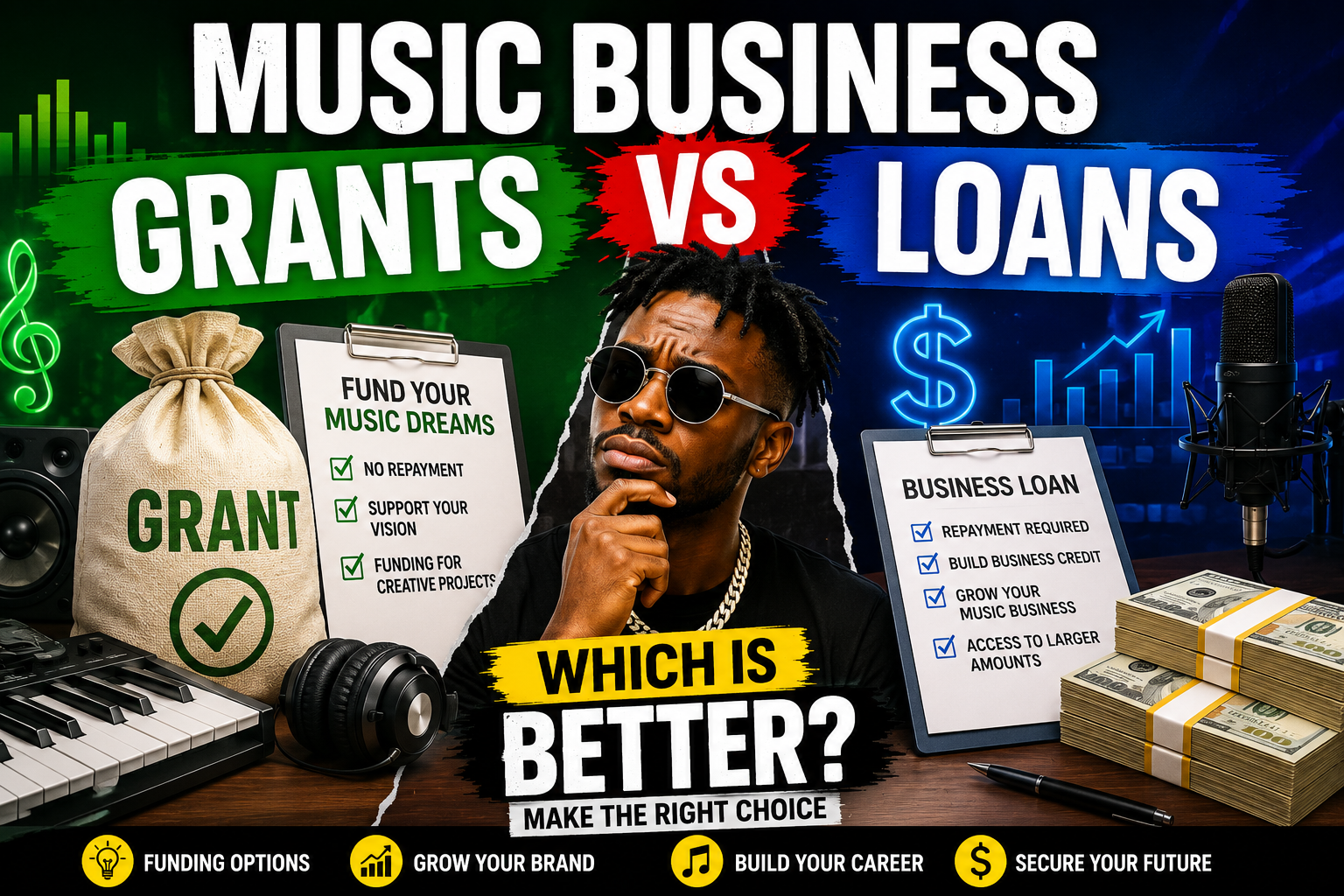

Every musician eventually hits the same wall. The songs are ready, the vision is clear, but the bank account tells a different story. At that point, two words start showing up in every conversation about growth: grants and loans. Both promise money. Both come with strings. Yet very few artists sit down and actually compare them side by side before choosing one. This article does exactly that, using real data, real programs, and real financial research, so you can decide which path fits your situation instead of guessing.

Understanding the Real Difference Between Music Business Grants and Loans

To start, a grant is money you do not pay back. A loan is money you must repay, usually with interest, on a fixed schedule. That distinction sounds simple, but it shapes everything else about how each option works in practice. Grants typically come from nonprofits, arts councils, foundations, or corporate giving programs that want to support culture and creative talent. Loans, on the other hand, come from banks, credit unions, or online lenders that exist to make a profit from interest.

Because of this, grants are often competitive and slow. According to Symphonic’s 2026 funding guide, grant funding can support recording, marketing, touring, and education, but most programs receive far more applications than they can fund, which means rejection is common even for strong projects [https://blog.symphonic.com/2026/01/07/grants-for-independent-musicians-2/]. Salt Lick Incubator, for instance, offers project-based grants ranging from $5,000 to $15,000 to artists working in melody- and lyric-driven genres, and recipients also get mentorship alongside the money [https://www.saltlickincubator.org/apply]. Creative Capital goes even further, offering unrestricted project grants up to $50,000 for artists creating bold new work across disciplines, including music [https://creative-capital.org/creative-capital-award/].

Loans move differently. Once approved, funds usually arrive faster, and you control exactly how the money is spent without a panel judging your artistic merit. However, that convenience has a cost attached, literally. A report by Crestmont Capital in 2026 found that the overall business loan default rate across all lender types sits at roughly 7.5%, though the figure ranges from under 2% for prime bank borrowers to over 25% for high-cost merchant cash advance recipients [https://www.crestmontcapital.com/blog/business-loan-default-rates-statistics-2026]. That range matters enormously for musicians, since most independent artists do not qualify for prime bank rates and often end up funneled toward the riskier, more expensive products.

What the Numbers Say About Musicians and Money

Before choosing either path, it helps to understand the financial reality most musicians already live in. According to the Music Industry Research Association’s 2018 survey of 1,227 musicians, conducted with the Princeton University Survey Research Center, the average American musician earns around $21,500 a year, and 61% said their music-related income is not enough to cover basic living expenses [https://www.digitalmusicnews.com/2018/06/27/music-industry-research-association-income-study/]. That single statistic explains why so many artists chase loans out of urgency rather than strategy. When rent is due and a session is booked, a loan can feel like the only fast option available.

Still, urgency is exactly where loans become dangerous. A study cited by Crestmont Capital, drawing on the Federal Reserve’s Small Business Credit Survey, found that roughly 22% of small businesses that applied for financing recently reported difficulty making payments on existing debt [https://www.crestmontcapital.com/blog/business-loan-default-rates-by-loan-type]. Musicians, whose income is often irregular and seasonal, face this risk more sharply than businesses with predictable monthly revenue. A slow month on tour or a delayed streaming payout can turn a manageable loan into a missed payment fast.

Grants avoid that repayment pressure entirely, but they demand something else: patience and preparation. Chartlex’s 2026 analysis of grant funding notes that artists who show strong streaming traction, such as consistent monthly listener growth, are more likely to win funding because panels use those numbers as proof of commercial viability [https://www.chartlex.com/blog/money/music-grants-funding-independent-artists-2026]. In other words, grants reward artists who already show momentum, while loans are available to almost anyone with acceptable credit, momentum or not. That single difference should guide a lot of your decision-making.

When a Grant Makes More Sense Than a Loan

Choosing a grant makes the most sense when your project has a clear, well-defined scope and you are not in immediate financial danger. Since grant panels evaluate proposals on planning and outcomes, not just talent, a scattered idea rarely gets funded. Programs like FACTOR in Canada, which awards between $5,000 and $30,000, and the PRS Foundation in the UK, which offers up to £15,000, both require applicants to describe exactly how the money will be spent and what success looks like at the end of the project [https://www.chartlex.com/blog/money/music-grants-funding-independent-artists-2026].

Grants also suit artists who value creative independence. Because there is no repayment obligation, a grant does not attach ongoing pressure to your release schedule or your royalty streams. This matters more than it sounds. Royalty advances, a popular alternative to both grants and loans, provide upfront cash in exchange for a share of your future earnings, and Symphonic’s guide points out that this arrangement can quietly reduce your income for years after the money is spent [https://blog.symphonic.com/2026/01/07/grants-for-independent-musicians-2/]. A grant carries no such long-term cost.

That said, grants are not instant solutions. Applications take real time to prepare properly, and most successful applicants were rejected somewhere along the way before winning their first award, according to Chartlex’s research into repeated grant applicants [https://www.chartlex.com/blog/money/music-grants-funding-independent-artists-2026]. So if your need is urgent, a grant cycle that opens in three months will not solve tonight’s studio invoice. Grants reward artists who plan ahead, not artists reacting to a crisis.

When a Loan Might Actually Serve You Better

On the other hand, a loan can be the smarter tool when timing matters more than cost. If a distribution deadline, a festival booking, or a video shoot depends on money arriving within days, waiting for a grant cycle simply is not realistic. Loans, particularly from credit unions or small community banks, tend to process faster and give you immediate control over the funds.

However, this speed only pays off if you borrow responsibly. Crestmont Capital’s research identified insufficient cash reserves as the leading cause of default, noting that 43% of businesses that defaulted in 2023 had fewer than two months of operating expenses saved before borrowing [https://www.crestmontcapital.com/blog/business-loan-default-rates-statistics-2026]. Musicians should apply that lesson directly. Before taking on debt, calculate whether your upcoming income, whether from shows, sync licensing, or streaming, can realistically cover repayment even during a slow month. Lenders call this the Debt Service Coverage Ratio, and most consider anything below 1.25 a warning sign [https://www.crestmontcapital.com/blog/business-loan-default-rates-by-loan-type].

Why Loans also make sense

Loans also make sense for artists building repeatable, income-generating infrastructure, such as home studio equipment or merchandise inventory that pays for itself over time. Unlike a one-time creative project, these purchases generate ongoing revenue that can service the debt naturally. Meanwhile, borrowing to fund a speculative single release, with no existing audience or distribution plan; is closer to the retail scenario. Crestmont Capital describes, where a business borrowed against uncertain future sales and ended up trapped in a debt spiral after the expected revenue never arrived [https://www.crestmontcapital.com/blog/business-loan-default-rates-by-loan-type]. The lesson transfers directly to music: borrow against a plan, not a hope.

Ultimately, neither option is universally better; each simply fits a different stage of an artist’s journey. A grant suits patient, project-based growth where the outcome can be clearly defined months in advance. A loan suits time-sensitive opportunities backed by a realistic repayment plan and existing income. Many successful independent artists actually use both at different points, applying for grants during quieter development periods while reserving loans for moments when speed truly matters.

Before you apply for either one, take three concrete steps. First, get real quotes for your project costs instead of estimating, since grant panels and lenders both respond better to precise numbers than rough guesses. Second, calculate your own debt service coverage ratio honestly, even if it means asking an accountant for thirty minutes of help. Third, build a simple funding calendar that tracks grant deadlines from organizations relevant to your genre, so you are never applying under pressure. Money will not fix a weak plan, but the right funding, chosen deliberately rather than out of panic, can turn a solid plan into a career that finally pays for itself.

[…] Music Business Grants vs Loans: Which Is Better? […]